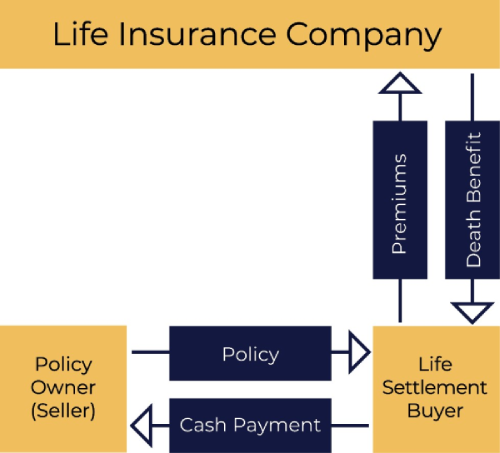

There are two sides of Life Insurance Settlement or Viaticals. There is the selling side. Later, we’ll discuss the buying or investment side later in Life Insurance Settements. However, if a policy holder is interested in selling their Life insurance they can do so. Have you’ve seen ads for life insurance settlements on TV, the radio or the internet? This way companies increase visibility for life insurance settlements as a solution for clients.

Often, life insurance settlement buyers advertise for direct business. In this manner, they aim to eliminate the competition. Therefore, providers say call them directly. They are the biggest, the best, and have investors backing them. Benefits to you, you get to keep 100% of the commission, etc. This sounds good, and we appreciate good marketing. Yet, that is not the complete life insurance settlement picture. For this reason, check out the Life Insurance Settlement Association in the link: LISA for further information.

In our market, buyers are known as “providers”:

- They do not have a fiduciary duty to clients to give the highest offer. In other words, I liken it when you try to buy a home. Here, you are not looking to pay the most amount of money, right?

- They may have many funds behind them (most of them do), but you do not know how many of those funds your client’s policy has been sent to. All of them? A few? One paying the provider the most money? Specifically, have the funds been leveraged against each other to obtain the highest offer? You don’t know, the process is not transparent.

- They allow agents and advisors to keep 100% of the sale commission. But, 100% of what? If the provider does not make an offer, 100% of zero is zero. Also, if the offer is low (and how do you know that it isn’t?), 100% of a low number is a low commission.

Whereas, life insurance settlements brokers (like us):

- We perform a fiduciary duty to you and your clients marketing their policy to obtain the highest amount of money for it that is possible.

- We access many different providers. Also, there are many funds behind them, which gives opportunity to place more clients’ policies. Maximizing value for clients’ policies. Therefore, more is better.

- We Leverage providers against each other. This allows us to obtain the highest offer for policies. Many providers see a policy equals competition, which increases leverage. Many times, providers make ever increasing offers on policies. They are driven higher by other providers.

- We Detail every offer a client’s policy receives in the sale contract. Commissions are disclosed in a detailed broker disclosure statement.

- Do share commission with agents and advisors? Many times the commission is higher with a broker, even with the commission share, because the offers are higher.

Case study:

A partner is closing on a client’s $350,000 universal life policy with no cash in it. The opening offer on the policy was $10,000. By the time we finished marketing it, the closing offer increased to $72,000. If an insurance agent went direct to a provider, the policy possibly sold for $10,000. The commission on $10,000 (up to $3,000), is much lower than the commission on $72,000 (up to $21,000), even with the broker commission share. To sum up, it is a win for the client, and win for the agent.

We are not implying that providers are bad or terrible. Simply put, they are important. They purchase clients’ policies. What we are saying is that life insurance settlement brokers maximize value for your clients and for you. There are no “comps” like in real estate. Unless you fully market a client’s policy, you will not know the true value of the policy.

We love to partner in life insurance settlements, we would honor being of service to you. We invite you to send your next case to the provider. Then, send us the case to us and we will see which way is best for you and your client. This way you can see the advantage of a life insurance settlement broker.

Feel free to contact me at 510-831-4754 or Michael@melfinservices.com

Michael Lien

California Insurance License: 0C39579

NPN: 1942573